ARV Meaning in Real Estate and Lending Explained

Understanding ARV meaning in real estate and how it impacts your loan can help you avoid surprises, set realistic expectations, and prepare a deal that makes sense for both you and the lender.

When you apply for a hard money loan, several numbers help shape how your deal is reviewed. Purchase price matters. Renovation costs matter. Your plan to sell or refinance also matters.

One number that connects all of those pieces is ARV.

ARV stands for after-repair value. It is the estimated value of a property once repairs and upgrades are finished. Investors often use ARV to think about profit. Hard money lenders use ARV to understand risk and decide how a loan should be structured.

What ARV Means in Simple Terms

ARV is what a property should be worth after the necessary work is done.

It is not the current value of the home. It is not a best-case guess. ARV is based on real sales of similar properties that have already been renovated and sold in the same or nearby areas.

For example, if updated homes in a neighborhood are selling for around $280,000, and your renovation plan brings the property to a similar condition and layout, then your ARV may be close to that amount.

Hard money lenders use ARV to understand what the property could reasonably be worth at the end of the project. That future value helps lenders decide whether there is enough room in the deal to support a loan.

Why ARV Matters in Hard Money Lending

Hard money loans are asset-based, which means the property itself is central to the lending decision.

Lenders use ARV to answer practical questions about the deal, including:

- What might the property be worth once repairs are complete?

- Is there enough value to support the loan amount?

- How much cushion exists if the project runs into issues?

These questions are not theoretical. Renovation projects often change as work begins. Unexpected repairs come up. Timelines stretch. Costs increase.

ARV helps lenders understand whether the deal can still work if things do not go exactly as planned. For loans through HardMoneyHome, ARV is reviewed alongside the purchase price, repair scope, and exit strategy to understand the full risk picture.

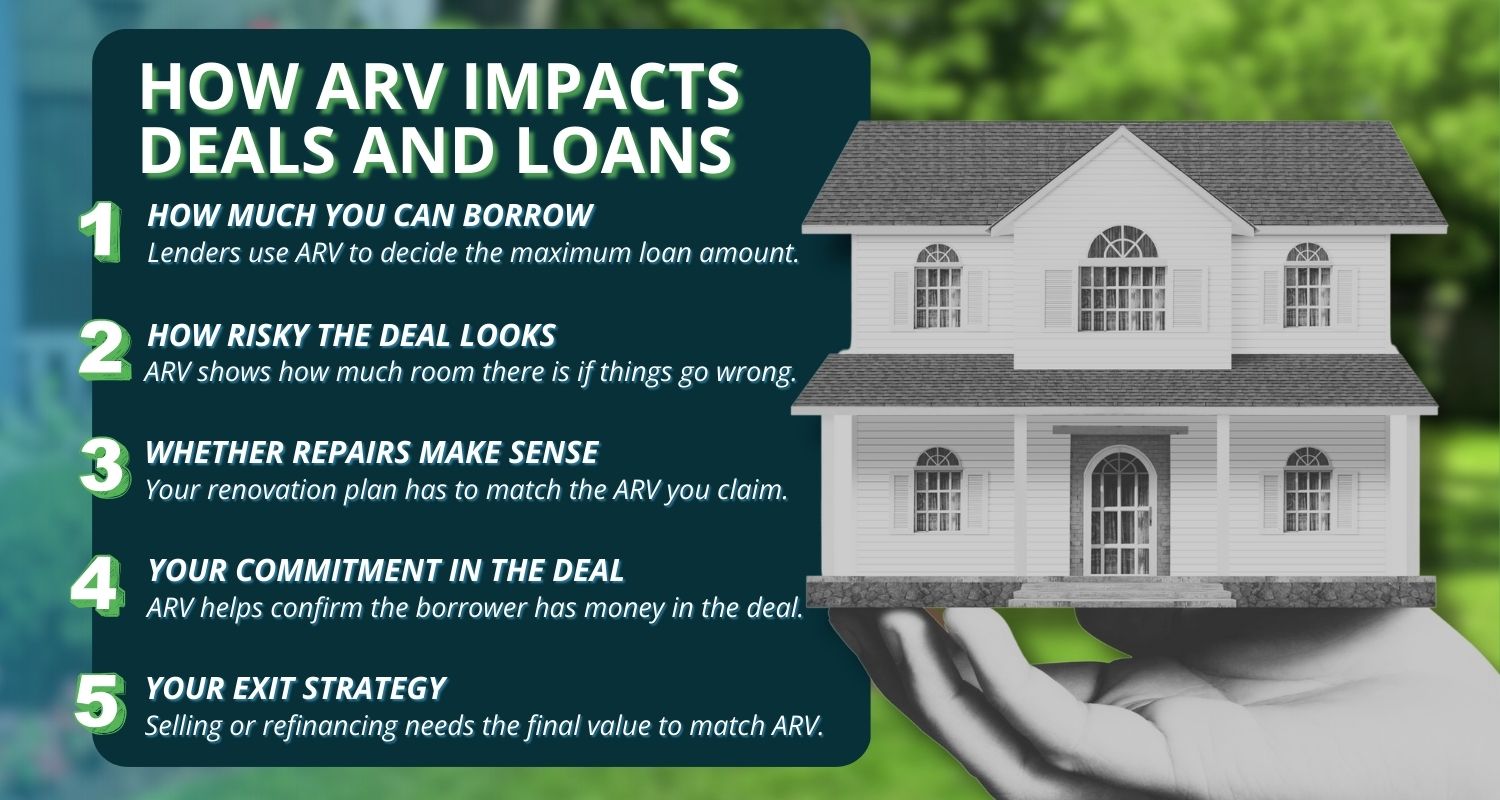

How ARV Impacts Your Loan Amount

Most hard money loans are structured using a percentage of ARV, often referred to as loan-to-ARV.

Instead of lending only based on what the property costs today, lenders look at what it should be worth after repairs. This approach helps balance opportunity with risk.

|

Loan Element |

How ARV Is Used |

|

Helps set a cap on how much can be borrowed |

|

|

Risk Control |

Leaves room if costs rise or timelines extend |

|

Borrower Equity |

Ensures the borrower has an investment in the deal |

|

Supports resale or refinance expectations |

Many hard money lenders operate within a range of about 65 to 75 percent of ARV.

This range allows for market changes, repair overruns, and delays without putting the loan at immediate risk.

If ARV estimates are aggressive or poorly supported, the lender may reduce the loan amount or request changes before moving forward.

ARV Is Reviewed With the Entire Deal

ARV is never reviewed in isolation.

Lenders also look closely at:

- Purchase price, to understand how much value is being created

- Repair budget, to confirm the work supports the ARV

- Timeline, to estimate holding costs and risk exposure

- Exit plan, to see how the loan will be paid back

All of these pieces should align. A strong ARV cannot make up for an unrealistic repair plan. A low purchase price does not help if the ARV does not reflect the local market.

Consistency across the deal is one of the biggest factors in whether a loan moves smoothly through underwriting.

How ARV Is Typically Calculated

ARV is usually supported by comparable sales, often called comps. Comps are recently sold properties that are similar to the one being renovated.

Lenders generally want comps that are:

- Similar in size and layout

- Located in the same neighborhood or nearby

- Renovated to a similar level of finish

- Sold recently enough to reflect current market conditions

Using strong comps shows that the ARV is grounded in real buyer behavior. Weak or outdated comps raise questions and often slow down the review process.

Lenders are not looking for perfection, but they are looking for reasonable comparisons that reflect what buyers are actually paying.

Common ARV Meaning Mistakes That Cause Problems

Overestimating ARV is one of the most common issues lenders see. This often happens when investors:

- Use the highest sale in the area instead of the typical sales

- Assume premium finishes without buyer demand

- Ignore neighborhood pricing limits

- Rely on future market appreciation

These assumptions may make a deal look better on paper, but they increase risk. When ARV inflates, loan amounts may need to decrease, or the deal may no longer qualify.

More conservative ARV meaning estimates usually lead to fewer issues and smoother funding.

ARV Versus Appraised Value

ARV and appraised value are related, but they serve different purposes.

An appraisal usually reflects what a property is worth in its current condition. ARV reflects what the property may be worth after renovations are complete.

For renovation-based hard money loans, lenders focus more on ARV because it represents the value expected when the loan is repaid or refinanced. This is why repair plans and comps are reviewed closely.

How ARV Affects Your Exit Strategy

Every hard money loan needs a clear exit strategy.

If the plan is to sell the property, ARV helps estimate whether the final sale price can cover the loan balance, closing costs, holding costs, and expected profit.

If the plan is to refinance, ARV helps determine whether long-term financing may be available once repairs are complete.

When ARV is realistic, exit strategies are easier to execute. When ARV is inflated, exits become harder and risk increases.

What Can Borrowers Do to Strengthen ARV Assumptions?

Borrowers who understand ARV tend to submit stronger loan requests.

Helpful steps include:

- Selecting realistic comparable sales

- Matching repairs to neighborhood expectations

- Avoiding pricing assumptions that buyers will not support

- Being ready to explain how you calculated ARV

This preparation helps lenders, including those with HardMoneyHome, review deals more clearly and efficiently.

Why Realistic ARV Assumptions Truly Matter

Realistic ARV assumptions are not about being conservative for the sake of caution. They help protect the deal over time.

When ARV is realistic, borrowers are less likely to face funding gaps if repair costs increase. Lenders are more confident that the property will support the loan even if the timeline extends.

Realistic ARV also makes exit planning clearer. Selling or refinancing becomes more predictable when the final value aligns with buyer demand rather than best-case scenarios.

At HardMoneyHome, deals built on grounded ARV assumptions tend to move faster and face fewer issues during funding and payoff.

Other Related Questions

How do hard money lenders evaluate real estate deals?

Hard money lenders look at the full deal, including the property, repair plan, timeline, and exit strategy. The goal is to understand whether the numbers and the plan make sense together. Not just whether one metric looks strong.

What types of properties can be financed with hard money loans?

Hard money loans are commonly used for fix-and-flips, rental properties, and distressed homes that may not qualify for traditional financing. Property condition and intended use often matter more than the borrower’s personal finances.

How do repair budgets affect loan approval?

Repair budgets help lenders understand how the property will reach its expected value. Unrealistic budgets or unclear scopes of work can raise concerns, even if the purchase price looks attractive.

When does refinancing with hard money make sense?

Refinancing with hard money is often used to bridge gaps, pull equity from an improved property, or transition between projects. Timing, property value, and exit plans all play a role in whether this strategy works well.

Conclusion

If you are evaluating a deal and want to understand how ARV meaning may affect your loan options, reviewing available lenders is often the next step.

HardMoneyHome is here to help borrowers explore hard money lenders based on deal type, location, and lending criteria. While HardMoneyHome does not fund loans directly, it provides a starting point for comparing lenders and understanding what different programs may require.

Taking time to match your deal with the right lender can help you move forward with clearer expectations and fewer surprises.