About Hard Money Loans

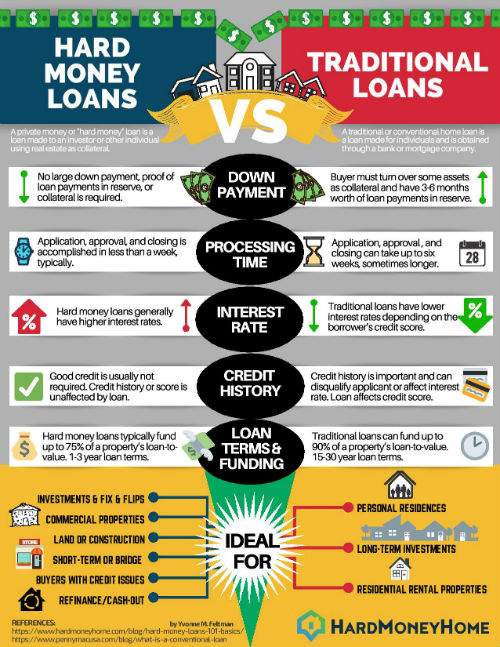

A private money or "hard money" loan is a loan made to an investor or other individual using real estate as collateral. Typically, the lender in these scenarios is an individual or private lending company as opposed to a bank or credit union and the borrower is most commonly a real estate investor who needs cash to purchase or rehab a property. Hard money loans are usually taken by borrowers who have been denied a loan by a traditional lending institution or who need to close a transaction more quickly than a bank will allow.

For these reasons, the rates and fees associated with such a loan tend to be higher than for a conventional mortgage. Additionally, hard money lenders may require the borrower to bring a significant amount of cash or equity to the closing in order to protect their interest in the event of a default. The terms for hard money loans also tend to be shorter than conventional loans, usually between 6 and 24 months in duration.

Top Cities

- Houston, TX

- Chicago, IL

- Brooklyn, NY

- Los Angeles, CA

- Miami, FL

- San Antonio, TX

- New York, NY

- Philadelphia, PA

- Las Vegas, NV

- Bronx, NY

- Phoenix, AZ

- Dallas, TX

- San Diego, CA

- Minneapolis, MN

- San Jose, CA

- Denver, CO

- Austin, TX

- St Louis, MO

- Indianapolis, IN

- Atlanta, GA

- Tucson, AZ

- Orlando, FL

- Portland, OR

- Seattle, WA

- Fort Worth, TX

- Jacksonville, FL

- Milwaukee, WI

- San Francisco, CA

- Cincinnati, OH

- Charlotte, NC

- Columbus, OH

- Cleveland, OH

- Fort Lauderdale, FL

- Sacramento, CA

- St Paul, MN

- El Paso, TX

- Louisville, KY

- Tampa, FL

- Memphis, TN

- Pittsburgh, PA

- Detroit, MI

- Albuquerque, NM

- Oklahoma City, OK

- Baltimore, MD

- Washington DC, DC

- Salt Lake City, UT

- Fresno, CA

- Buffalo, NY

What Is A Hard Money Loan?

Simply defined, a hard money loan is a short-term loan that is secured by real estate from a non-traditional lender (i.e. not a bank, credit union, etc.). Hard money lenders are usually private investment firms. The amount of a hard money loan depends on the value of the collateral property.

Basically, a hard money loan is an alternate way to borrow money without going through traditional bank mortgage lenders. Most hard money property loans come from individuals, investors or groups of investors.

Hard money is an option for those who need funding fast and for those who may not qualify for traditional long-term bank loans. It is important to understand how these types of loans work.

What are the Advantages of a Hard Money Loan?

There are a number of reasons why residential property buyers and commercial buyers and builders seek out hard money loans. Some ways that hard money is different than a bank loan include:

- Faster application, approval and loan processing

- Provide more financing for distressed property in need of repairs or renovations

- Property value has most clout, individual financial history or credit is not as important for approval

- Less paperwork and requirements from application start through the end of the loan term

Using a hard money lender is beneficial because the focus is not on the ability of repayment. Instead, more concern is for the value of the collateral, or property. Hard money loans are short-term loans lasting anywhere from 1- 5 years depending on the lender.

How Can I Qualify for a Hard Money Loan?

Bank loans require excellent credit in order to offer a low interest rate rate, but great credit is not necessary for a hard-money loan. A cash contribution of 20 to 40 percent of the property or project costs will need to be supplied by the borrower.

Financial records such as bank, retirement and investment statements, pay stubs, driver's license, social security card and other documentation depending on marital status is required. For those who are self-employed, two years of past tax return statements and business banking statements may be required.

In addition, depending on the property type, a business plan for the project, including a budget for renovation costs, title statements and property assessments may have to be included. Banks require more extensive paperwork, while hard money lenders require less.

Where Can I Get a Hard Money Loan?

For those seeking hard money loans, they can be obtained from hundreds of private financial firms both small and large. Many of these lenders can be found locally or online by the click of a mouse, but it is important to research for complaints and compliance.

Sometimes the existing property owner may be able to provide financing for the investment, or fix and flip deal. Local banks, credit unions and large nationwide banks also offer real estate loans.

Another place to obtain a loan is through an existing mortgage. Current homeowners who have built up enough equity in their home can apply for a home equity loan or line of credit (HELOC). This can allow the buyer to borrow up to 80 percent of the equity value against their primary residence. Being that your primary residence is used as the collateral in this transaction, it can be a more risky way to secure financing for those who are inexperienced property investors.

Different Types of Hard Money Loans

There are several different ways hard money can be loaned including:

- Fix and Flip Loans

- Investment Property Loans

- Bridge Loans

- Cash Out Refinancing Loans

- Commercial Loans

- Construction Loans

There are similarities between each of these and some of the names are used interchangeably in the real estate and financial industries.

Bank-issued loans for terms of 15 to 30 years can be used to purchase long-term non-owner-occupied properties in good condition. These loans offer lower interest rates than hard money private lenders.

Government sponsored lender Fannie Mae, offers a HomeStyle Renovation Mortgage for single-family one-unit investment properties, units in condos, co-ops, mobile homes and planned unit developments (PUDs). Any renovation or repair is eligible, as long as it is permanently affixed to the property and completed within a year of the loan issue.

In some cases the party selling a property can offer a loan to the buyer. Other non-conventional ways of funding a loan is by partnering with someone who has the cash, receiving a loan from friends or family, borrowing from a retirement account or 401k, taking out a personal or business loan or home equity loan or line of credit (HELOC).

Hard Money Loans vs Traditional Loans

How is hard money different than traditional loans? There are three main areas:

Flexibility. Hard money lenders do not use a typical bank underwriting process so agreements can be more flexible than traditional loan agreements. Negotiations regarding terms and requirements can be a lot less stringent with a hard money lender than a bank.

Approval. Since the most critical factor is collateral, the lender will provide financing typically up to 85 percent of what the property is worth. Those who have a foreclosure or negative events on their credit report will find a hard money lender is much more forgiving than a bank lender.

Speed. Hard money loans close quickly in comparison to other loans. The application process of a hard money loan can take a few days. In contrast, a bank mortgage application can take weeks to complete due to the financial records and documentation required.

In addition, the approval process for a bank loan can take a month or more. With hard money lenders, the approval process often takes less than a week. Experienced buyers or builders who have an established a relationship with a hard money lender can get through the process even quicker than new borrowers.

Hard Money Loan vs Bridge Loan

Frequently referred to as hard money, a bridge loan often finances a property that may be in transition and does not yet qualify for traditional financing. Bridge loans are short-term loans used until other permanent loan financing can be secured. A bridge loan allows the borrower to fulfill current obligations or property rehabilitation by providing immediate cash flow.

Similar to hard money loans, these loans have higher interest rates and are usually backed by some form of collateral, such as real estate. These loans can be issued through a bank or privately and the term is a few weeks, up to one year.

Properties Good For Hard Money

Several property types can benefit from a hard money transaction. There are various scenarios where hard money can be used as a tool to get the buyer to arrive at their end-goal whether it be owning an investment, a primary residence, or some other scenario. Properties suitable for these transactions are aplenty:

- Single-family homes

- Multi-unit homes

- Duplexes or split residences

- Condominiums

- Commercial Projects or Major Equipment

- New Construction

Another type of property that is gaining in popularity is private residential travel lodging or homestays. These properties are purchased with the intent to rent out all or part of the property daily, weekly or monthly as accommodation for visiting travelers. Popular travel booking websites showcase these short-term, privately owned rental properties.

Example of a Typical Hard Money Loan Scenario:

Marilyn and John are a young professional couple wanting to increase their savings and start building wealth. They stumble upon a foreclosed condominium home for sale that they feel would be a good fix-and-flip project. The property was last purchased for $195,000, but the bank is willing to sell for $115,000.

The couple believes that a $35,000 investment will create a property that will sell for $195,000 after repairs. A hard money lender agrees with their ARV estimate and is willing to lend them 70%, or $136,500. John and Marilyn use the loan proceeds to purchase the home and pay for half the rehab. They allow the lender to put a lien on the property and they contribute $19,500 to complete the project. If the property goes on the market and sells for $195,000 or more, they will clear a profit of $39,000, which is a 200% return on their $19,500 contribution.

Recent Topics

View All

Types of Foreclosure

In the United States, there are generally two kinds of foreclosure processes to consider, judicial foreclosure and non-judicial foreclosure. States typically make the rules about which type will be in play on a given property but in some states both types are possible so it is important to understan...

Read More

5 Steps in Obtaining a Hard Money Loan

It may seem obvious, but nobody just googles the term "hard money loan" and gets the money they need for a home or remodel. There is a process to follow, as with any loan. The fact that hard money loans are faster and require less paperwork than a standard mortgage from big banks does not mean that...

Read More

Legitimate vs Predatory Lenders

Anytime a borrower seeks out alternative or special financing, like a hard money loan, it is extremely important to do the homework. Everyone considering a hard money loan should know what to expect, how to evaluate the options presented and what kinds of documentation will be expected at closing. ...

Read MoreView By State

- Alaska

- Alabama

- Arkansas

- Arizona

- California

- Colorado

- Connecticut

- Washington DC

- Delaware

- Florida

- Georgia

- Hawaii

- Iowa

- Idaho

- Illinois

- Indiana

- Kansas

- Kentucky

- Louisiana

- Massachusetts

- Maryland

- Maine

- Michigan

- Minnesota

- Missouri

- Mississippi

- Montana

- North Carolina

- North Dakota

- Nebraska

- New Hampshire

- New Jersey

- New Mexico

- Nevada

- New York

- Ohio

- Oklahoma

- Oregon

- Pennsylvania

- Rhode Island

- South Carolina

- South Dakota

- Tennessee

- Texas

- Utah

- Virginia

- Vermont

- Washington

- Wisconsin

- West Virginia

- Wyoming

Your Information is Processing

Your Information is Processing