About Commercial Hard Money Loans

Commercial hard money loans are asset-backed loans that are secured by real estate. In these lending scenarios, the borrower is usually an individual or business who needs to purchase or take cash out of equity in a commercial building and the lender is typically a private company that specializes in higher-risk loans. These types of loans can be made on any type of commercial property, including office buildings, warehouses, large residential housing units, and special-use properties like restaurants, churches, and barber shops. They generally carry higher rates of interest than conventional bank loans but can be very helpful for borrowers who need to have access to cash quickly or who have lower credit ratings and therefore do not qualify for traditional loans.

Top Cities

- Houston, TX

- Chicago, IL

- Brooklyn, NY

- Los Angeles, CA

- Miami, FL

- San Antonio, TX

- New York, NY

- Philadelphia, PA

- Las Vegas, NV

- Bronx, NY

- Phoenix, AZ

- Dallas, TX

- San Diego, CA

- Minneapolis, MN

- San Jose, CA

- Denver, CO

- Austin, TX

- St Louis, MO

- Indianapolis, IN

- Atlanta, GA

- Tucson, AZ

- Orlando, FL

- Portland, OR

- Seattle, WA

- Fort Worth, TX

- Jacksonville, FL

- Milwaukee, WI

- San Francisco, CA

- Cincinnati, OH

- Charlotte, NC

- Columbus, OH

- Cleveland, OH

- Fort Lauderdale, FL

- Sacramento, CA

- St Paul, MN

- El Paso, TX

- Louisville, KY

- Tampa, FL

- Memphis, TN

- Pittsburgh, PA

- Detroit, MI

- Albuquerque, NM

- Oklahoma City, OK

- Baltimore, MD

- Washington DC, DC

- Salt Lake City, UT

- Fresno, CA

- Buffalo, NY

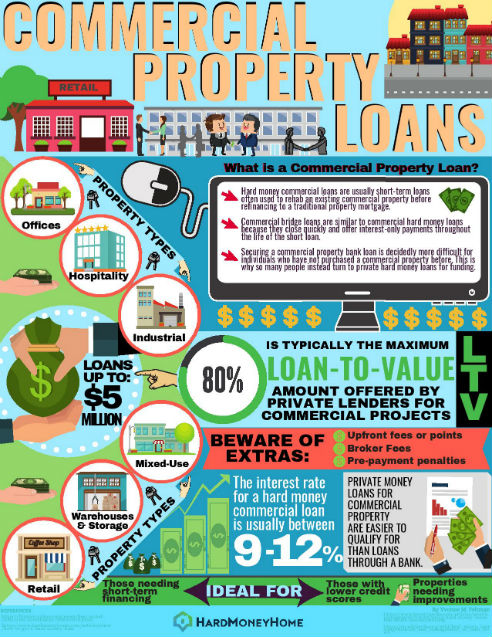

What is a Commercial Hard Money Loan?

Hard money loans for commercial real estate (CRE) can be secured faster and with less paperwork than conventional commercial bank loans. These types of loans are used specifically for business purposes and are short-term loans.

These loans are often used to rehab an existing commercial property before refinancing to a traditional property mortgage. The interest rate for a hard money commercial loan is usually between 9 and 12 percent and lasting no longer than a few years. Commercial bridge loans are similar commercial hard money loans because they close quickly and offer interest-only payments throughout the life of the short loan.

When looking to buy commercial real estate, you simply can't go to the bank and get a traditional mortgage like you would for a residence. Securing a commercial property bank loan is decidedly more difficult for individuals who have not purchased a commercial property before. This is why so many people instead turn to commercial hard money loans for funding.

Commercial Property Types

There are a number of different property types suitable for a commercial hard money loan. Often times a property that actively produces income, such as a hotel, self-storage, or multi-unit property is a preference for lenders. There is an array of other property types that fall into the commercial category, including:

- Industrial and Warehouses

- Office complexes

- Storage centers

- Hospitality properties (hotels, resorts, etc)

- Duplexes, apartments and multi-family homes (as investment properties)

- Mixed-use buildings

- Retail

Perks of a Commercial Hard Money Loan

Commercial hard money loans are becoming the go-to for those who need commercial funding because of the many perks offered. These include:

Easier to Qualify. Sometimes banks have a lot of requirements that rule out some buyers. This is not the case with hard money lenders who have a less stringent application and approval process.

Fast Approval. Traditional loans can take weeks to process thus delaying business progress. In hard money lending, the commercial property is evaluated more than the buyer which streamlines the process. The commercial property's loan to value ratio is the main factor that hard money lenders consider.

Flexible Process. The strict underwriting process of traditional loans does not apply to commercial hard money loans. Each situation is assessed on a case-by-case basis which offers much more flexibility.

No cash out limits. This can buffer the risks involved with other loans if the buyer is unable to get financing in time.

Ways To Fund Commercial Real Estate

There are a plethora of choices when it comes to funding commercial real estate, these include: private investors, pensions, insurance companies, secured acquisitions, refinances, cash-outs, bridge loans, construction loans, 504 SBA loans, SBA 7(a) loans, HUD loans, Fannie Mae, Freddie Mac, fixed rate and floating rate, non-recourse and recourse loans, commercial mortgage-backed securities (CMBS), 2nd mortgages, mezzanine loans, and preferred equity loans. Peer-to-peer lending platforms are gaining popularity and can also be used to fund a commercial property project.

Despite this large array of options, many buyers are increasingly partnering with private hard money commercial lenders due to the easy, faster process. Although interests rates can be a bit higher, it makes up for other hassle-factors involved in the traditional commercial mortgage process.

Who Uses Commercial Hard Money?

- Private investors and estates

- Real estate entities

- Partnerships

- Trusts

- Corporations

- LLCs

- Delaware Corporations

- Foreign nationals

Where to Get a Hard Money Commercial Loan

Private commercial finance companies are in abundance and can be discovered by a quick internet search. These lenders can exist in one area or be operating throughout the country. It is important to do research and evaluate these lenders and consider the following:

- Upfront fees, also called origination fees or points. These add to the loan amount and can be as high as 6 percent.

- Broker fees. Many of the commercial lenders found online use third-party lenders whose fee is rolled into your loan fees. Be sure to investigate this as fees aren't usually higher than 6 percent.

- Prepayment penalties. These are not standard, so you'll want to go with a lender who does not impose a prepayment fee if possible.

Residential Loans vs Commercial Loans

The term of commercial loans is typically shorter than that of a residential loan. Commercial real estate loans last a few years, up to 20 years with a longer amortization period. For example, a commercial loan could have a term of 9 years with an amortization period of 25 years. The investor would make payments for 9 years as if they were making payments on a 25 year loan, but at the end of 9 years, one "balloon" payment of the entire outstanding loan balance would be the final payment on a commercial loan.

Residential mortgages are typically made to individuals while commercial loans are often made to business entities such as trusts, developers, partnerships and corporations. Often these are formed for the specific purpose of acquiring commercial property. An entity may not have credit history, in which case the lender may require the principals of the entity to guarantee the loan. This provides the lender with whom they can hold accountable in the event of loan default. However, if this type of guaranty is not required by the lender, and the property is the only means of recovery in the event of loan default, the loan is called a non-recourse loan, which means the lender has no recourse against anyone or anything other than the property.

Commercial Construction Loans vs Commercial Loans

A commercial construction loan is used to finance the costs associated with new construction, renovations or remodeling of a commercial property. This funding can be used to pay for labor and materials for the construction of a new property, the purchase and development of land for a new commercial property, or the renovations of existing properties.

Construction loans are not received in a lump sum up front. Instead, the borrower will work with the construction loan lender to create a draw schedule. This means that specific funding amounts will be released as the project hits new phases. For example, the first draw will be for the land clearing and development. The next draw might occur when the foundation is set. Another draw will be released when the framing, or structure is complete, and so on.

Fix and Flip Commercial Hard Money Loans

A fix and flip, or rehab commercial loan is typically used to buy a foreclosed commercial property, also known as an REO (real estate owned), from a bank. These bank-owned commercial properties can be purchased for significantly less than their fair market value. Banks are very reluctant to make fix and flip commercial loans. Lenders who close the most commercial fix and flip loans are private hard money lenders. Most hard money lenders will loan a buyer around 60% of the purchase price of the REO.

The total cost of the project will include the purchase price of the REO, the cost to fix up the property, plus the commission of the lease. A commercial fix and flip lender will typically loan up to 65 percent of the total project costs. Sometimes, a commercial fix and flip hard money loan is cheaper as a construction loan.

SBA Commercial Real Estate Loans

Unlike various other commercial property loans, financing for commercial real estate offered by private companies and guaranteed by the Small Business Administration (SBA) makes up an SBA loan. SBA loan guarantees were created by Congress to stimulate growth of small businesses. The SBA 7(a) program is a 25-year, fully-amortized, first mortgage loan program with a floating rate.

The SBA 504 loan program begins with a fixed-rate, first mortgage and then adds a 20-year fully-amortized, SBA-guaranteed, second mortgage behind it. This is the most common way to get a fixed rate SBA loan. Many SBA lenders will write conventional construction loans that convert automatically to 25-year SBA loans at the end of the first term.

Recent Topics

View All

What is a Deed of Trust?

A deed of trust, also called a trust deed, is a document that represents a real estate purchase where there is a loan involved. Many people who have a deed of trust simply refer to it as their mortgage or their home loan. But having a deed of trust is technically a little bit different from that. ...

Read More

Types of Foreclosure

In the United States, there are generally two kinds of foreclosure processes to consider, judicial foreclosure and non-judicial foreclosure. States typically make the rules about which type will be in play on a given property but in some states both types are possible so it is important to understan...

Read More

Legitimate vs Predatory Lenders

Anytime a borrower seeks out alternative or special financing, like a hard money loan, it is extremely important to do the homework. Everyone considering a hard money loan should know what to expect, how to evaluate the options presented and what kinds of documentation will be expected at closing. ...

Read MoreView By State

- Alaska

- Alabama

- Arkansas

- Arizona

- California

- Colorado

- Connecticut

- Washington DC

- Delaware

- Florida

- Georgia

- Hawaii

- Iowa

- Idaho

- Illinois

- Indiana

- Kansas

- Kentucky

- Louisiana

- Massachusetts

- Maryland

- Maine

- Michigan

- Minnesota

- Missouri

- Mississippi

- Montana

- North Carolina

- North Dakota

- Nebraska

- New Hampshire

- New Jersey

- New Mexico

- Nevada

- New York

- Ohio

- Oklahoma

- Oregon

- Pennsylvania

- Rhode Island

- South Carolina

- South Dakota

- Tennessee

- Texas

- Utah

- Virginia

- Vermont

- Washington

- Wisconsin

- West Virginia

- Wyoming

Your Information is Processing

Your Information is Processing